California has shifted firmly into a buyer’s market after four straight months of year-over-year inventory growth. In simple terms, there are now more homes for sale than there are buyers.

According to real estate analyst Nick Gerli, “no one is buying homes in California.” Sales have dropped to levels just below those seen during the Great Recession. With home prices still sky-high and mortgage rates hovering near 7 percent, many buyers are staying out of the market.

Related posts

Why It Matters

The pandemic dramatically changed California’s housing landscape. Remote work allowed many to leave big cities like San Francisco and Los Angeles, either moving to smaller towns or leaving the state. Though prices dipped briefly in early 2020, they quickly rebounded and have climbed steadily since.

Now, those high prices—paired with steep mortgage rates and economic uncertainty—are holding back demand. Tariffs under President Donald Trump are also contributing to the state’s economic unease.

What To Know

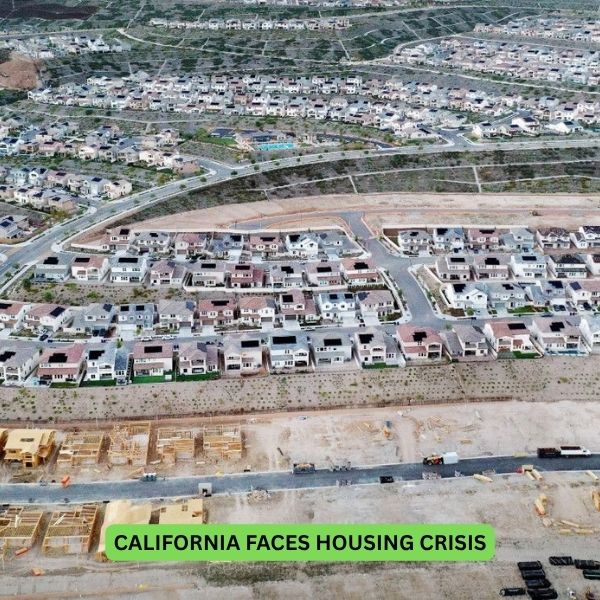

Realtor.com reports that California had 73,160 active listings in May, the most since October 2019. Nationwide, housing inventory rose over 30 percent year over year in May, and California followed that same trend.

Oscar Wei, deputy chief economist at the California Association of Realtors, noted that this inventory growth is seasonal. Listings usually increase from March through August as families try to settle before the new school year. However, he said this growth could level off in June.

California cities like Riverside, Sacramento, Los Angeles, Anaheim, and Oakland are among the top 50 U.S. metros with the largest gap between sellers and buyers, according to a Redfin study.

While more inventory should be good news for buyers, interest remains low. California recorded about 25,100 home sales in April. That’s up 1.6 percent from the year before, but still 20 percent below the long-term average and 40 percent below the pandemic peak.

Wei explained that high borrowing costs and insurance issues are discouraging home purchases. Gerli added that this weak demand is now driving prices down. Home values in California fell by 0.42 percent in April—the fourth straight month of decline.

“Prices are dropping because low demand is now being met with rising inventory,” Gerli said. While supply was tight for years, it’s now surging.

The Bigger Picture

Even with slight monthly drops, California homes remain expensive. The average home value was $796,255 in April, up 1.3 percent from a year earlier. The median sale price reached $854,700, rising 0.2 percent year over year. Five years ago, that number was $571,000.

Price cuts are becoming more common, seen in 34.8 percent of home sales—up 10.2 percent from last year. On the flip side, homes selling above list price fell to 40.3 percent, down nearly 10 percent year over year.

What People Are Saying

Oscar Wei believes that many buyers are waiting for lower prices or mortgage rates, which may dip slightly by the end of the year. He also said the market may have already peaked for the year.

Hannah Jones of Realtor.com said California’s price surge during the pandemic has priced many out. Wolf Richter pointed out that demand has “essentially collapsed.” Even with modest new listings, unsold homes are stacking up.

Lance Lambert said more markets are moving beyond the inventory shortfall of the Pandemic Housing Boom. Redfin’s Asad Khan noted that sellers are slow to adjust to this new buyer’s market, but rising days on market and fewer showings may soon change that.

What Happens Next

Home prices are expected to dip slightly by year’s end. Zillow projects declines in 31 California cities, including San Francisco (-5.2 percent), San Jose (-3.8 percent), Sacramento (-3 percent), Los Angeles (-1.2 percent), and San Diego (-0.7 percent).

Wei anticipates mild monthly drops driven by seasonal patterns and increased supply. Despite volatility in some areas, he still expects a modest year-over-year price increase overall for the state.

{kind=link}